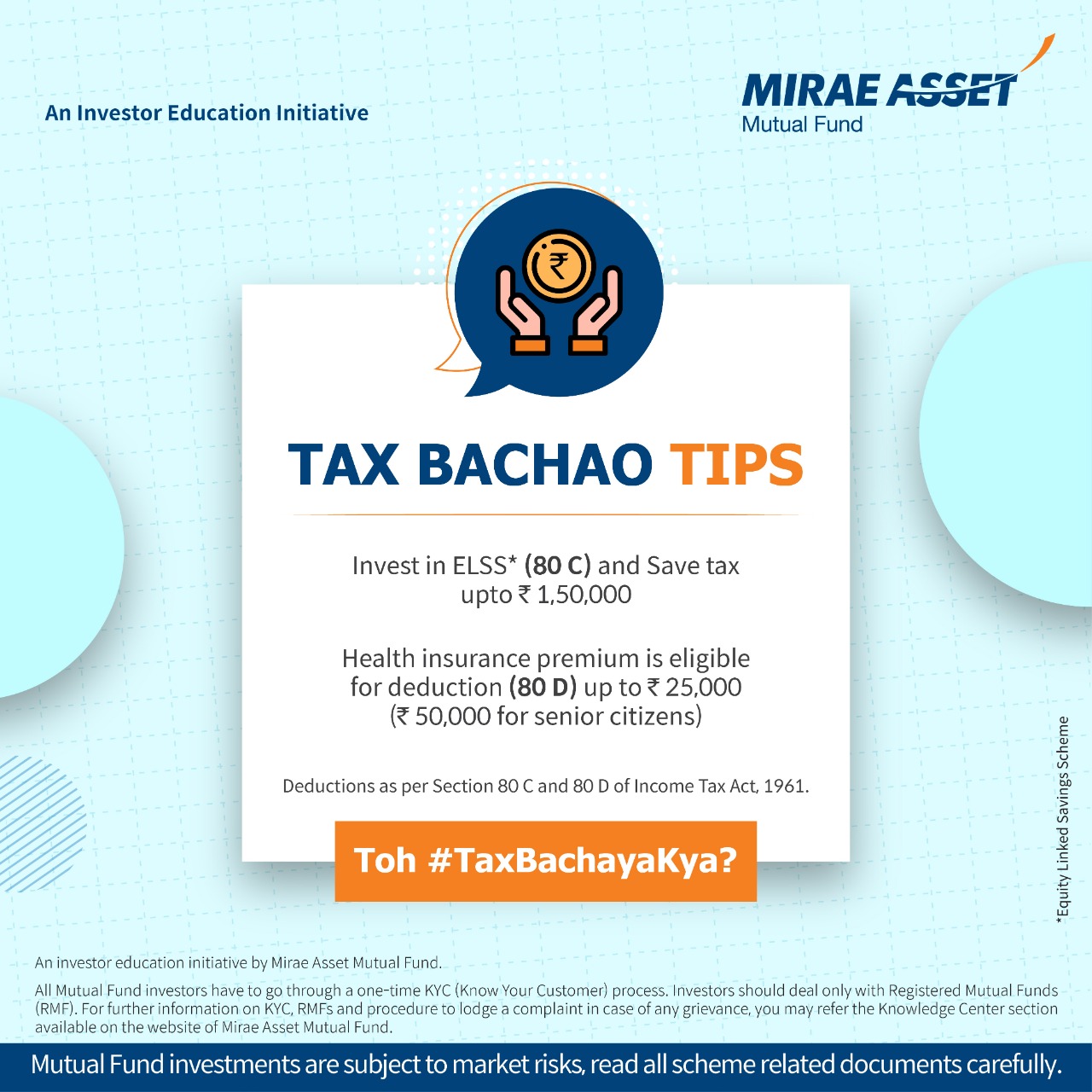

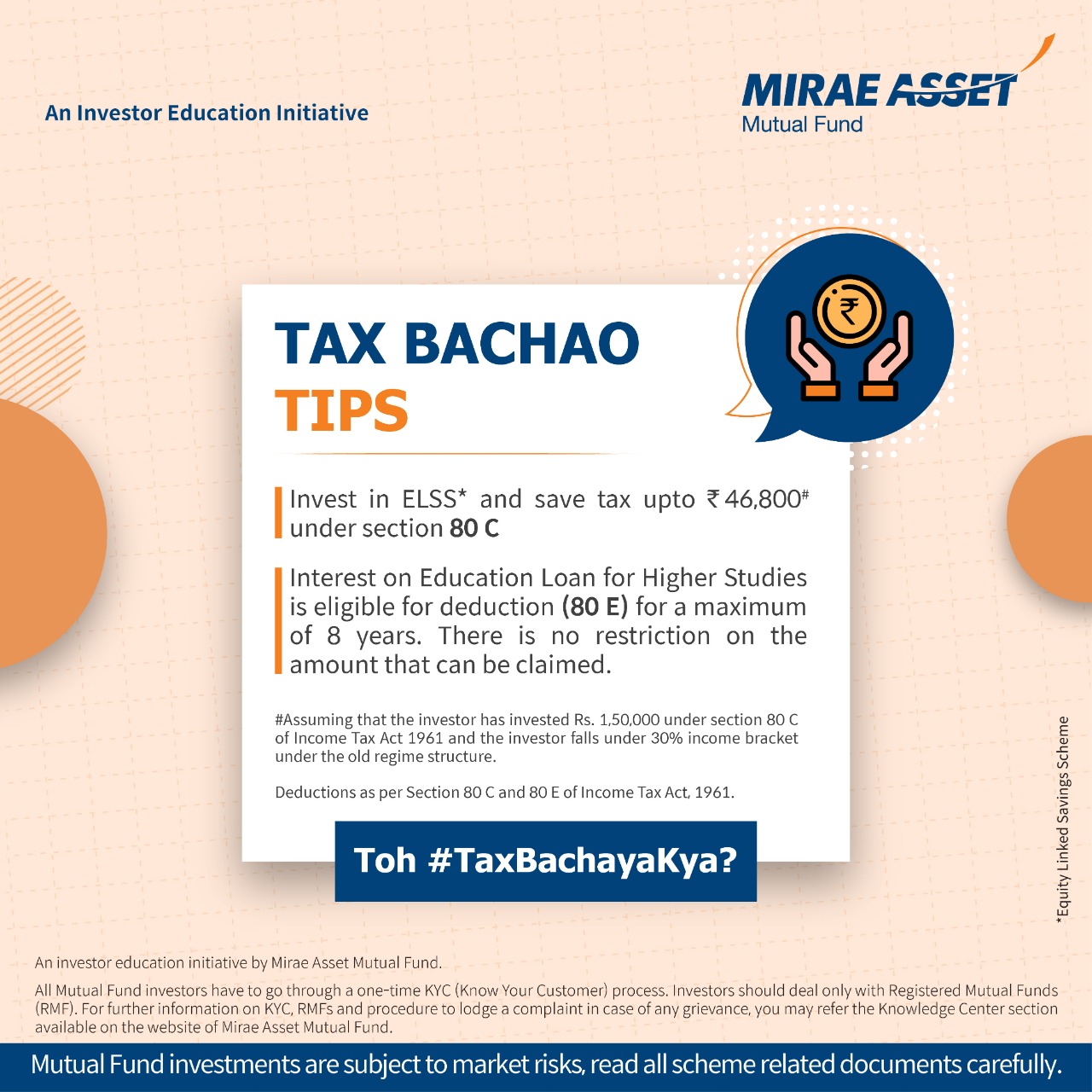

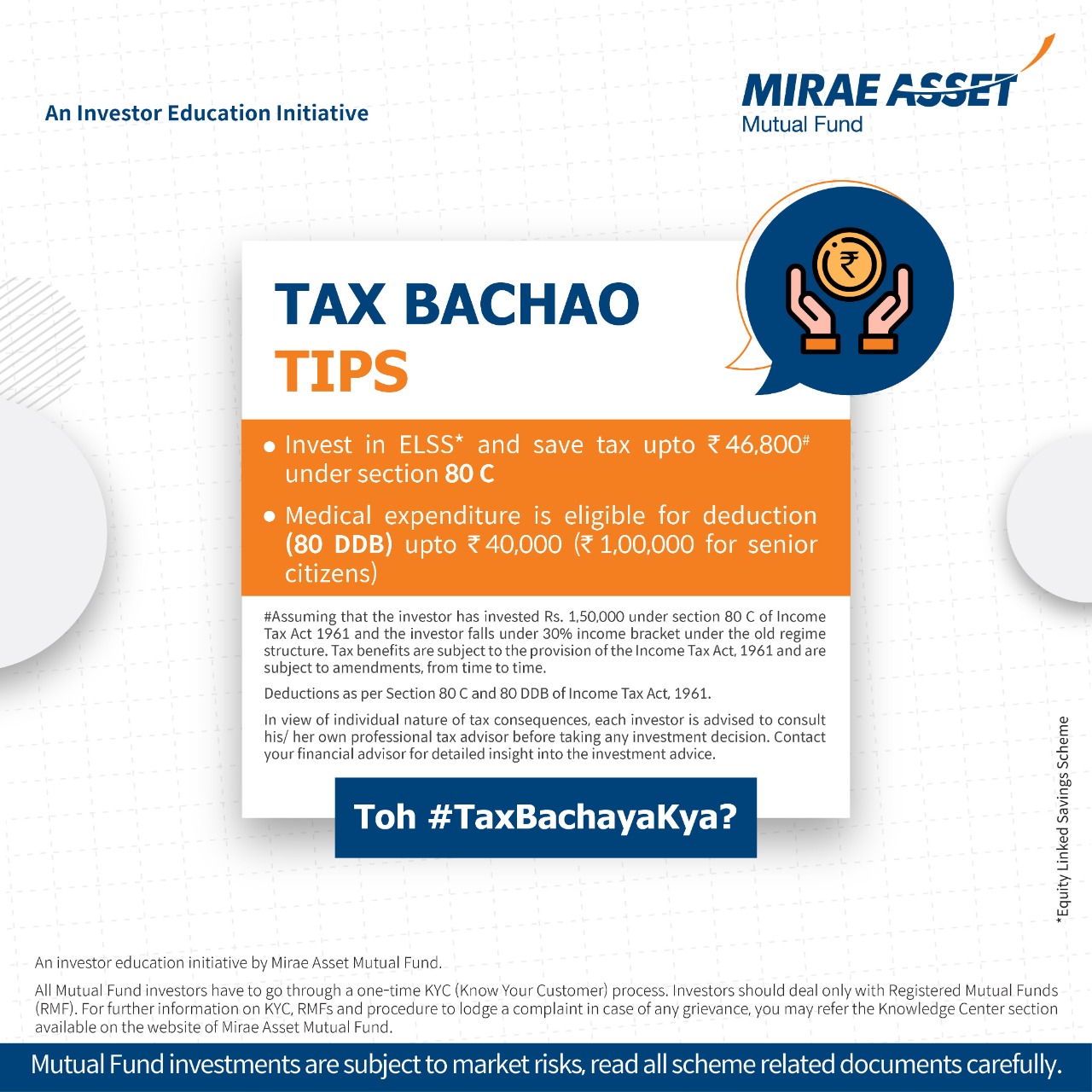

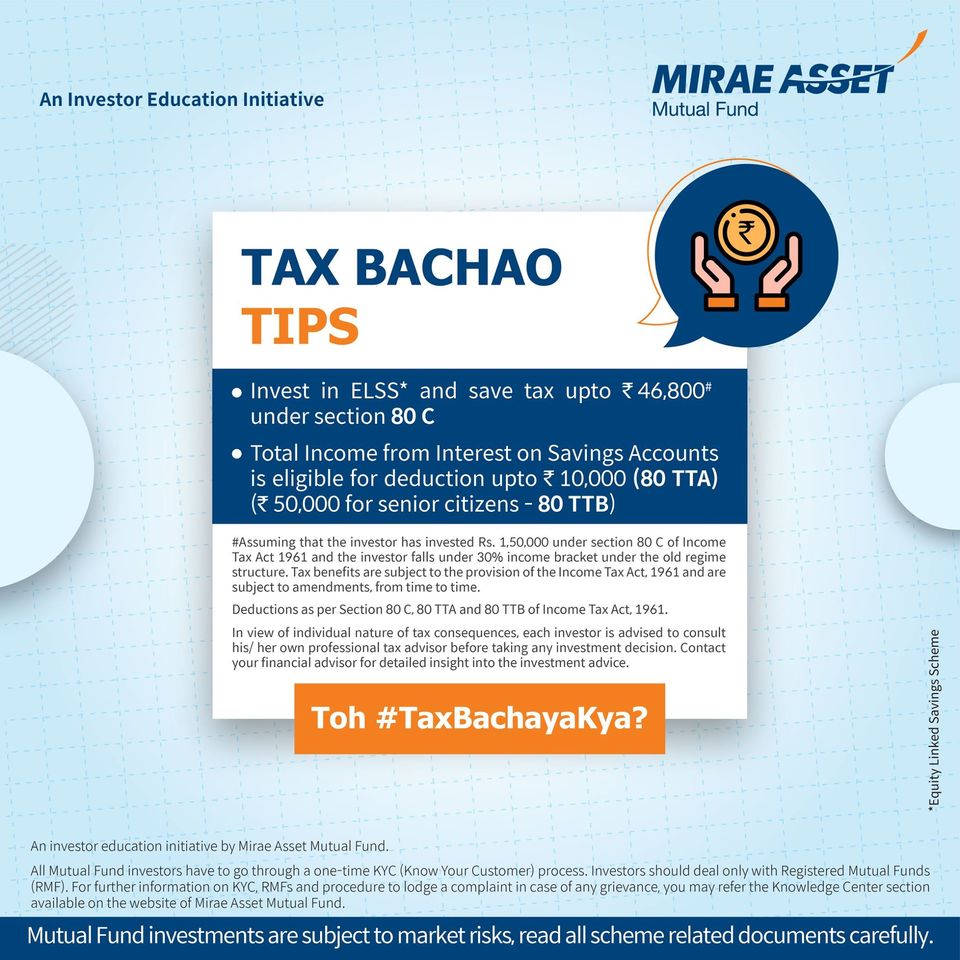

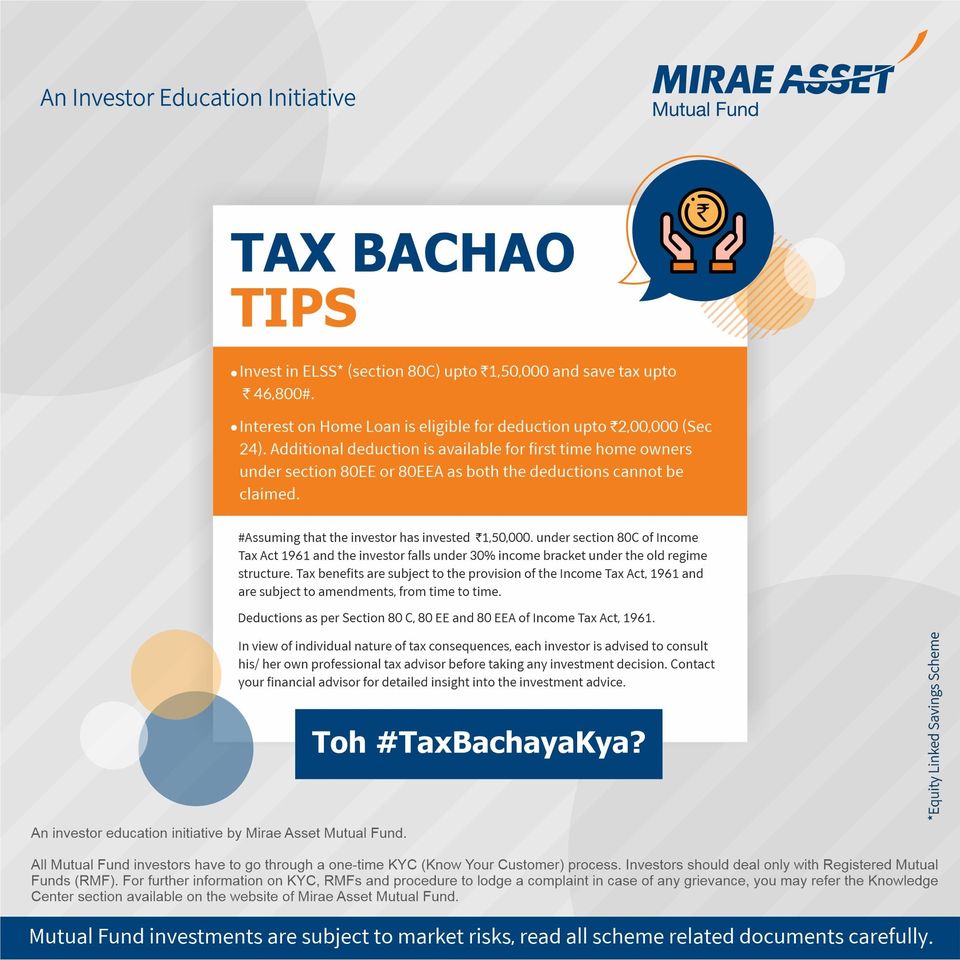

Tax Bachaya Kya?

By investing in ELSS (Equity Linked Savings Schemes) you can now save tax and aim to create wealth through equities. Section 80C of Income Tax Act 1961 allows tax payers to reduce their income tax obligations by investing in specified eligible investments like ELSS. The amount you invest can be claimed as deduction from their taxable income for the purpose of income tax computation when filing your returns. Your 80C investments should also not be made only for the purpose of tax savings, but it should also be linked to your financial goals.

Advantage of ELSS

Equity Linked Savings Schemes (tax saver mutual funds) are also among the most tax friendly investment schemes among the eligible Section 80C investment options. There is no taxation during the investment period, unlike many fixed income 80C investment options. Since ELSS are equity oriented schemes with a minimum investment period of three years, capital gains from Equity Linked Savings Schemes up to Rs 1 lakh in a year is tax exempt. Capital gains in excess of Rs 1 lakh in any financial year is taxed at 10%. Dividends paid by ELSS funds are also tax free in the hands of the investors

.jpg)