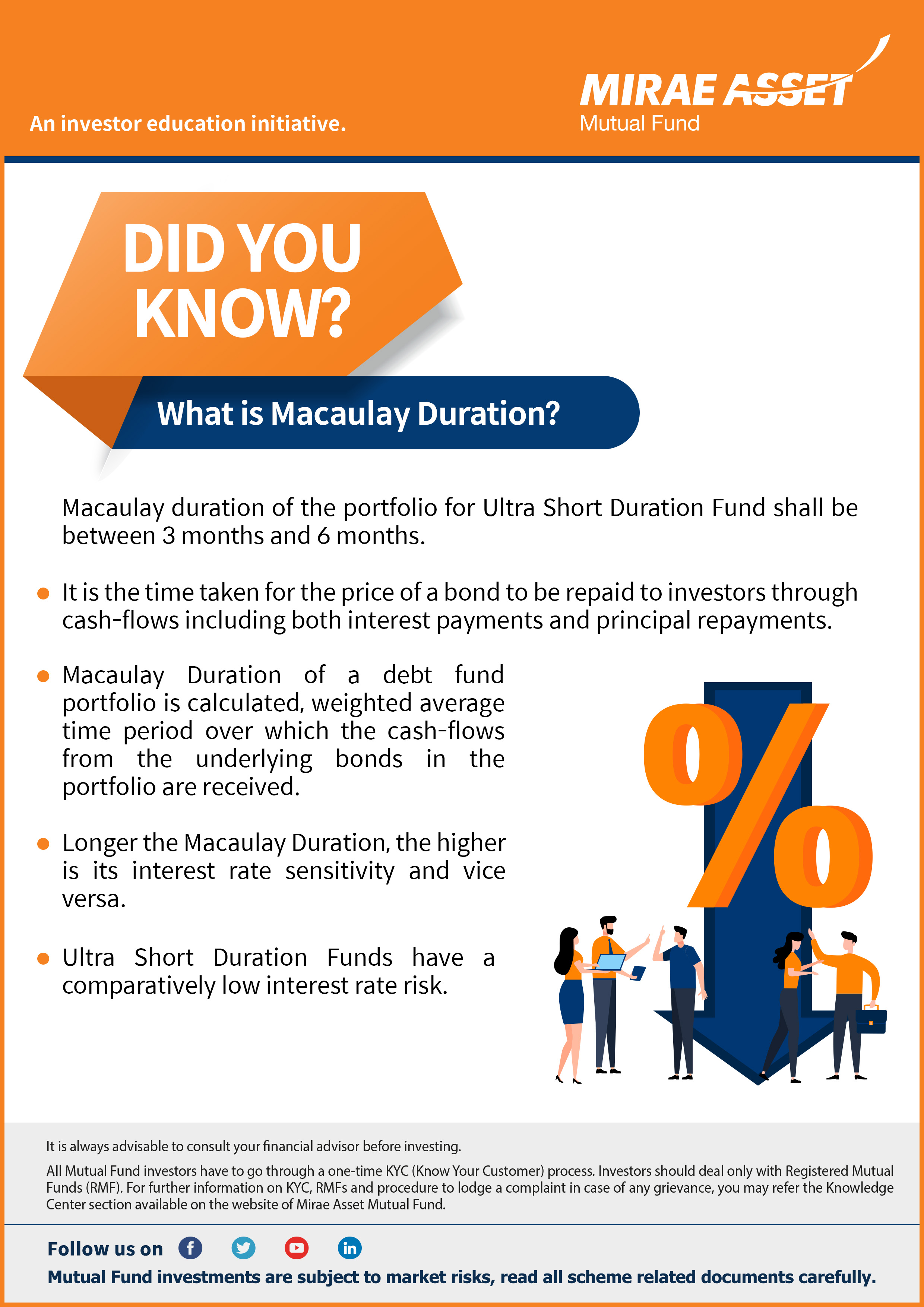

Ultra short duration funds are fixed income mutual fund schemes which invest debt and money market securities such that the Macaulay Duration of the scheme portfolio is 3 months to 6 months. These funds are suitable for short term investments

since they are less volatile and aim to produce more stable income compared to funds with longer duration profiles. Many investors get confused between liquid funds and ultra-short duration funds.

Difference between liquid fund and ultra-short duration fund

The main difference between liquid fund and ultra-short duration fund is the maturity or duration profile of the two schemes. Liquid funds invest in debt or money market instruments which mature in 91 days, while Macaulay Duration of ultra-short duration funds is 3 to 6 months. The yield curve is usually upward sloping. For example, as on 15th September 2020, the yield of 3 month (maturity) Government Securities (G-Sec) is 3.31%, while that of 6

month G-Secs is 3.52% and 1 year G-Secs is 3.72% (source: worldgovernmentbonds.com). Therefore, ultra-short duration funds usually seek to give higher returns compared to liquid funds. However, since the durations of these funds are longer

than liquid funds, they can be slightly more volatile than liquid funds on a daily or weekly basis. Therefore, you need to have longer investment tenures for ultra-short duration funds.

Who should invest in ultra-short duration funds?

These funds are suitable for conservative investors who can remain invested for at least 3 months - up to 1 year. Please note that ultra-short duration funds do not guarantee capital safety or assure returns. You need to have appetite for

daily or weekly volatility. However, if your investment horizon is longer than 3 months, then probability of making a loss is lower. Further, please note that, if your investment horizon is 1 year or longer then there may be more suitable

investment options.

Why should you invest in ultra-short duration funds?

Many investors, who have surplus funds which they may not need in the next 3-12 months may keep these funds parked in their savings bank account. You can put such idle money to productive use i.e. get potential returns, by investing it for

3 – 12 months in ultra-short funds. Savings bank interest rates of major PSU and private sector banks are currently in the range of 2.75 – 3.5%. Ultra-short duration funds have the ability to generate higher returns compared to your savings

bank interest rate. In fact current (last 3 months) ultra-short duration fund returns on an annualized basis are nearly 90 – 150 bps higher than even 6 – 9 months FD rates of major banks (Source: Advisorkhoj Research and policybazaar.com

data as on August 2020).

Taxation of Ultra-short duration funds

If your investing holding period is less than 36 months, then the capital gains arising from the sale of units of ultra-short duration funds will be added to your income and taxed according to your income tax slab rate.

Factors to consider while investing in ultra-short duration funds

- Investment Tenure: Your investment tenure for these funds should be 3 – 12 months. If your investment tenure is less than 3 months, then liquid funds may be better investment options. If your investment tenure is more than 12 months,

then you may find better investment options in debt funds.

- Low expense ratio: Since the yields of ultra-short duration funds are relatively low compared to longer duration funds, higher expense ratios will eat into returns. You should invest in funds which have comparatively lower expense

ratios.

- High credit quality: There is a misconception among some investors that there is no risk in ultra-short duration funds. Investors should know that, even though these funds have low interest rate risk, they are subject to credit

risks. You should also understand that credit risk can result in permanent reduction of your investment. You should invest in funds which are of high credit quality, i.e. high allocations to AAA / A1+ rated papers. You can find out

the credit quality of a scheme from the monthly fund factsheets.

- Do not select a scheme on the basis on short term performance:Bond yields keep changing because of macro-economic conditions, RBI’s monetary policy, exchange rate and other market related factors. You should not form returns expectations

based on short term performance. Also, a scheme can give higher returns because it took more credit risks. You should evaluate risk factors, your own risk appetite, investment tenure, credit quality of the scheme, expense ratio etc.

and make informed investment decisions.

- Performance track record of the fund manager / fund house: Look at long term performance track record of the fund manager to see if he / she is able to outperform his / her peers consistently across different market / interest rate

conditions. More importantly, look at the performance track record of fund house across other schemes (in different categories).

Conclusion

You can make your surplus funds work for you to seek to generate returns, by investing them in ultra-short duration funds instead of keeping it idle in your savings bank account. You should discuss with your financial advisors, if ultra-short

duration funds are suitable for your short term investing needs.

Disclaimer:

An Investor Education and Awareness Initiative by Mirae Asset Mutual Fund. All Mutual Fund investors have to go through a one-time KYC (Know Your Customer) including the process for change in address, Phone number, bank details, etc. Investors should deal only with registered Mutual Funds details of which can be verified on SEBI website (https://www.sebi.gov.in) under ‘Intermediaries /Market Infrastructure Institutions’. For further information on KYC, RMFs and procedure to lodge a complaint in case of any grievance, you may refer the Knowledge Centre section available on the website of Mirae Asset Mutual Fund. Investors may lodge complaints on https://www.scores.gov.in against registered intermediaries if they are unsatisfied with the responses. SCORES facilitate you to lodge your complaint online with SEBI and subsequently view its status.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

ETF Website

ETF Website

Global

Global

Australia

Australia

Hong Kong SAR

Hong Kong SAR

India

India

Korea

Korea

UAE

UAE

United Kingdom

United Kingdom

United States

United States

Vietnam

Vietnam

Brazil

Brazil

Colombia

Colombia

Japan

Japan

Singapore

Singapore

Ireland

Ireland

Canada

Canada

.jpg)

.jpg)